End2end Knowledge Vault

Trusted supply chain truth — defined, referenced, and translated into practical playbooks by End2End experts.

Access additional resources and insights

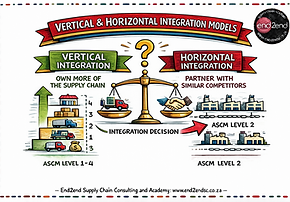

Vertical and Horizontal Integration Models

Last revised date:

11 March 2026

Integration is a strategic choice about where you compete and what you own. This guide contrasts vertical vs horizontal integration models, shows how to choose the right option, and maps the implications to SCOR, KPIs, and CSCP exam cues.

Vertical and Horizontal Integration Models: When to Own, Partner, or Consolidate

Integration is a strategic choice about where you compete and what you own. This guide contrasts vertical vs horizontal integration models, shows how to choose the right option, and maps the implications to SCOR, KPIs, and CSCP exam cues.

Definition (ASCM) + plain-language translation

ASCM uses the term *vertical integration* to describe how far a firm stretches across consecutive, value-adding stages - from upstream inputs through to downstream customer delivery. In plain language: **how much of the chain you own and run yourself**.

ASCM uses *horizontal integration* to describe expansion at the same stage of the value chain - producing/selling similar products across markets, frequently through a horizontal merger. In plain language: **how much you scale by combining with peers at the same level**.

Important exam nuance: these are *strategy and operating model* choices (ownership/control). They are not the same as “systems integration” (ERP interfaces) or “internal/external supply chain integration” (process collaboration).

This short explainer video is a fast strategy-level refresher on how firms expand through horizontal integration (combining with a competitor at the same level of the value chain) versus vertical integration (moving upstream or downstream to own/control more stages of the supply chain). It’s useful for CSCP revision because it frames the decision as a scope-and-control choice: scale and market power vs. coordination, quality/availability control, and margin capture—then reinforces the logic with simple examples and a quick pros/cons recap.

Integration model taxonomy (what “counts” in practice)

Most real-world supply chains sit on a **spectrum** - from arm’s-length buying, to long-term partnerships, to joint ventures, to full ownership. CSCP-style questions often present a single move (buy/own/merge) and ask you to classify it.

Vertical integration models

Backward integration: owning or controlling activities upstream (e.g., acquiring a supplier or building an in-house component plant).

Forward integration: owning or controlling downstream activities closer to the customer (e.g., acquiring a distributor/retailer, building your own DC network, or launching direct-to-consumer).

Full vs tapered integration: full means you make/own most of the stage; tapered means you do some in-house *and* still buy/sell externally (useful for benchmarking and surge capacity).

Quasi-integration / captive models: tight control without full ownership (exclusive contracts, dedicated capacity, tooling ownership, vendor-managed inventory, consignment, or minority equity stakes).

Virtual integration: orchestrating the chain through design authority, data, standards, and strong governance rather than assets (common in electronics and platform businesses).

Video about Vertical Integration overview:

Horizontal integration models

Horizontal merger/acquisition: combining with a competitor (same level) to expand scale, market share, footprint, or capability.

Consolidation/roll-up: repeated acquisitions to build a larger network (common in logistics and distribution).

Capability acquisition: buying a peer for a specific capability (e.g., cold-chain, last-mile, digital fulfilment).

Joint venture / strategic alliance: shared ownership and risk to access a market, technology, or capacity.

Horizontal collaboration: peers cooperate without merging (e.g., shared transport lanes, pooled warehousing, shared forecasting for a category).

Keiretsu-style integration model

Keiretsu-style networks sit in the middle ground between pure market outsourcing and full ownership integration.

Unlike vertical integration, where a firm internalises upstream or downstream stages under one balance sheet (control via ownership), a keiretsu achieves coordination through embedded relationships—long-term partnering, preferential dealing, shared improvement routines, and sometimes financial ties (e.g., cross-shareholdings or a coordinating bank/trading-company core in the classic Japanese form).

Unlike horizontal integration, which expands scale by combining with or acquiring peers at the same tier (control via consolidation and market power), keiretsu strengthens competitive position by building an ecosystem advantage across tiers—stability, quality learning, and capacity access—without fully merging entities.

The trade-off is governance: vertical integration concentrates execution risk inside the firm, horizontal integration can raise competition/regulatory concerns, while keiretsu can create lock-in and opacity if competitive tension disappears and resilience options (alternates, modularity, exit routes) aren’t deliberately designed.

If you want a quick, plain-language grounding before diving into the supply-chain implications, this short video gives a clean overview of what a keiretsu is, where it comes from, and why the model can create both advantage and fragility. It explains the “networked” nature of keiretsu groups (e.g., long-term partnerships, cross-shareholding, and a coordinating finance core), then balances the benefits (stability, collaboration, risk-sharing, smoother supply continuity) against the downsides (reduced competitive tension, potential opacity, and slower adaptation). Use it as a fast primer—then link it back to your SRM decisions: where embedded relationships improve quality/continuity, and where they create lock-in and concentration risk.

Why it matters (service, cost, cash, risk)

Integration decisions reshape your supply chain’s performance profile and your balance sheet.

The impact shows up fast in four areas:

Service

Improved reliability when you eliminate handoffs and align priorities across stages.

Faster lead times when you control capacity and scheduling end-to-end.

Cost

Potential economies of scale/scope, fewer transaction costs, and less duplication.

BUT higher fixed costs and higher “cost of complexity” if you integrate a messy operation.

Cash

Ownership usually increases working capital and capital employed (plants, DCs, fleet, systems).

That makes ROIC and cash conversion cycle as important as unit cost.

Risk

Reduced exposure to supplier/distributor failure, but increased exposure to your own operational execution risk.

Horizontal integration can reduce competition risk for you, but can increase regulatory/antitrust risk.

How it shows up (symptoms)

Use these as a quick diagnostic to spot when an integration conversation is likely to surface:

Upstream pain (pushes toward backward integration or stronger supplier governance)

Critical material shortages, chronic quality escapes, IP leakage, or single-source bottlenecks.

High expediting costs, unstable lead times, and recurring line stoppages.

Downstream pain (pushes toward forward integration or tighter channel control)

Poor service visibility, high chargebacks/claims, channel conflict, or customer experience issues.

Margin leakage to intermediaries, weak demand signal, or inability to shape assortment/pricing.

Peer-level pain (pushes toward horizontal integration/collaboration)

Network inefficiency from subscale operations (empty miles, low utilisation, duplicated overheads).

Need for rapid footprint expansion, new lanes/markets, or capability gaps that are slow to build.

Root causes and drivers (what usually sits underneath)

Practitioner reality: integration is rarely “a procurement decision”. It’s normally driven by one or more of these economics and control realities:

Strategic control

Protecting a differentiating capability (quality, speed, IP, customer experience).

Reducing dependence on a bottleneck supplier, logistics node, or dominant channel partner.

Transaction cost economics (make-or-buy logic)

When contracts can’t fully specify performance (uncertainty) and assets are highly specific (special tooling, dedicated lines), coordination through the market gets expensive - so internalisation can win.

Where assets are generic and markets are competitive, outsourcing/partnering typically stays advantaged.

Scale and scope

Horizontal integration aims to create economies of scale (lower unit cost via higher volume) and scope (shared overheads, shared assets).

Vertical integration can remove double-margins and reduce coordination losses, but may also create internal bureaucracy.

Risk posture

Volatile geopolitics, supplier fragility, and long lead times can shift the “right” model over time.

Regulation can push either way (e.g., localisation requirements vs competition enforcement).

How to measure (simple diagnostic + what good looks like)

Before debating “buy a supplier” vs “merge with a competitor”, run a short, numbers-first diagnostic. This keeps decisions grounded in end-to-end economics.

**Step 1: map the value chain and profit pools.** Identify where margin is earned and where service is won or lost.

**Step 2: quantify true cost-to-serve (not just unit cost).** Include variability costs: expediting, safety stock, quality failure, obsolescence, chargebacks, and lost sales.

**Step 3: model ownership scenarios with ROIC.** Add capex, ramp-up, transition costs, working capital, and integration overhead.

**Step 4: stress-test risk.** Evaluate single points of failure, concentration risk, and time-to-recover under disruption.

**What good looks like:** the chosen model improves service and resilience while meeting your hurdle rate (ROIC) and keeping complexity manageable.

How to improve (playbook steps)

Use this practical playbook to choose the right integration model and execute cleanly:

Clarify the intent: growth, resilience, quality, speed, cost, market access, or customer experience.

Choose the control point: which stage must you control to win (specification, capacity, data, channel)?

Screen the options on a spectrum: contract improvements → partnership/JV → minority stake → acquisition/build.

Build the business case: TCO + cost-to-serve + ROIC + risk-adjusted value (include integration cost).

Design the operating model: decision rights, KPIs, planning cadence (S&OP/IBP), master data, and governance.

Execute the transition: Day-1 readiness, change management, systems/process integration, and talent retention.

Stabilise and optimise: remove duplicate overheads, harmonise policies, and lock in synergies with controls.

SCOR lens (where integration decisions land)

Map integration choices to SCOR so teams know *where to act* and *what to change*:

Plan

Define the integration strategy, investment logic, and policies (make/buy, inventory, service).

Update IBP/S&OP to include capacity ownership decisions and channel strategy.

Source

Backward integration changes supplier segmentation, contracting, and SRM - your “supplier” may become an internal plant.

Even without ownership, use quasi-integration levers (dedicated capacity, VMI, supplier development).

Transform

Own/manufacture decisions drive network design, manufacturing strategy, quality systems, and asset utilisation KPIs.

Integrate planning parameters (lead times, yields, batch sizes) into enterprise planning.

Fulfill

Forward integration affects DC strategy, last-mile capability, order promising, returns handling, and customer experience.

Expect cost-to-serve redesign and channel conflict management.

Orchestrate

Set governance, performance management, data standards, and cross-functional decision rights.

Manage risk, compliance, and synergy tracking across the enlarged enterprise.

CSCP exam cues (what gets tested + common traps)

Expect questions that test classification and trade-offs. Typical cues:

Exam cues

Acquiring a supplier = backward vertical integration; acquiring a distributor/retailer = forward vertical integration.

Merging with a competitor at the same stage = horizontal integration (often a horizontal merger).

If the scenario emphasises “owning multiple stages from raw material to consumer”, choose vertical integration.

Watch for distractors: diversification (different products/industries) vs horizontal integration (same stage/similar products).

Benefits often tested: coordination, reliability, margin capture, economies of scale/scope. Risks tested: capex, complexity, antitrust, loss of flexibility.

End2End practitioner notes (what consultants do in reality)

Integration succeeds or fails in execution. In client work, we focus on a few non-negotiables:

Practitioner notes

Synergy realism: separate “paper synergies” from executable synergies; assign owners and timelines.

Operating model first: clarify decision rights across Plan/Source/Make/Deliver before touching systems.

Data discipline: harmonise item masters, suppliers/customers, and planning parameters early - bad data kills integration.

Talent retention: protect critical planners, buyers, and plant/DC leaders; integration churn destroys service.

Policy alignment: unify service promises, inventory policies, and customer allocation rules to avoid internal conflict.

Change management: the best economics fail if teams don’t adopt the new cadence, KPIs, and escalation paths.

Practical examples (quick scenarios)

**Backward integration:** A manufacturer buys a specialised component supplier after repeated quality escapes and long lead-time shocks. The win comes from tighter process control and faster engineering changes - not just cheaper parts.

**Forward integration:** A brand launches direct-to-consumer fulfilment to control customer experience and demand data. The hidden work is cost-to-serve design and returns management.

**Horizontal integration:** Two regional distributors merge to create national coverage. The value is network density and shared overheads, but the risk is customer churn during system and policy harmonisation.

**Horizontal collaboration (no merger):** Competing carriers share linehaul capacity on backhauls to reduce empty miles. Governance and data-sharing rules matter more than the lane plan.

Related Articles:

Explore related articles that deepen the concept, connect the SCOR processes, and sharpen your practical application.

End-to-End Supply Chain Planning Stack: Strategy to Execution |

Demand Analysis → Demand Management Loop: Turning Signals into Decisions (and Decisions into Learning) |

Performance and Continuous Improvement |

Keiretsu-Style Networks: |

Supply Chain Flows and Echelons |

Supply Chain Through the SCOR Lens (SCOR DS) |

Vertical and Horizontal Integration Models |

Product Life Cycle (PLC) |

Supply Chain Maturity |

The Bullwhip Effect |

Safety Stock |

Cheat Sheet

Integration Models - Cheat Sheet:

Vertical integration (ASCM): extent to which a company performs multiple value-adding stages internally (raw materials through to sale to end customer).

Backward integration (ASCM): buying/owning upstream elements toward raw material suppliers.

Forward integration (ASCM): buying/owning downstream elements toward consumers.

Horizontal integration (ASCM): producing/selling similar products across markets at the same stage; often via a horizontal merger.

Horizontal merger (ASCM): consolidation of two or more competing firms into one.

Drivers: control, reliability, margin capture, scale, market access, resilience.

Metrics: cost-to-serve, lead-time variability, OTIF, ROIC, working capital, risk concentration.

Best first moves: partner/JV, long-term contracts, dedicated capacity, supplier development before full ownership.

Traps: capex + complexity, ROIC erosion, integration disruption, antitrust risk (horizontal).

Vertical and Horizontal Integration Models

Quotes of Wisdom

“In supply chains, ownership doesn’t create integration - decision rights do. Assets only amplify the discipline you already have.” — End2End Supply Chain Academy

Definitions: ASCM. (2025). ASCM Supply Chain Dictionary (19th ed.) [Reference]. Accessed 2026-02-21.

EPM. (6 September 2022). Horizontal Vs Vertical Integration [Video]. YouTube. Accessed 2026-02-21. https://www.youtube.com/watch?v=YNLC40hup_I

Educationleaves. (15 April 2025). What is Keiretsu? Definition, Advantages, Disadvantages #keiretsu [Video]. YouTube. Accessed 2026-02-22. https://www.youtube.com/watch?v=GSoYnDyq8QQ

Article Sources

Category:

SCOR Process:

Level:

Strategy & Network Design

Plan, Source, Transform, Fulfill, Orchestrate

Exam-Ready

Last Updated:

11 March 2026 at 10:42:42